My idle thoughts on tech startups

Chewy S-1: Category Leadership + Conveyor Belt Into Consumers’ Homes

This post also appears on NextView’s blog.

Chewy has rapidly grown from a startup to a multi-billion commerce company, establishing itself as the leader in pet e-commerce. Chewy sells tens of thousands of products from many 3rd party brands, as well as its own private label brands (though latter remains <10% of sales). The company launched in 2011 and then was acquired by PetSmart for over $3 billion in 2017 (PetSmart itself owned by PE firm BC Partners), but Chewy is now preparing for life as a standalone public company.

I’ll break down Chewy’s business based on their recent S-1 filing here. I know some of the investors in Chewy prior to the PetSmart acquisition, but I am not a shareholder nor do I intend to purchase shares in the IPO. But the company is of particular interest to me given NextView is an investor in and I’ve been a board member of Grove Collaborative, another large and rapidly growing company in the consumer CPG space with a recurring purchase model.

Is Chewy Still a Rapidly Growing Business?

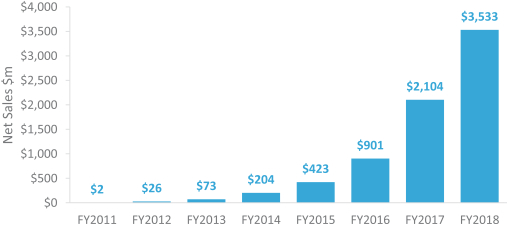

A $3.5B revenue business still growing >50% YoY? Check.

Embedded Growth From Existing Customers

One of the key features of Chewy’s business is the recurring nature of customer purchases. Consumers typically own a pet (or pets) for many years, so they are continuously purchasing food, toys, and accessories for their pet for an extended period.

Chewy now has over 10 million customers, repeat purchases by existing customers account for approximately 90% of their revenue today. But importantly Chewy keeps growing, even without acquiring any new customers, because their existing customers spend more money with them. This is analogous to SaaS companies like Slack or Dropbox, which have strong revenue growth just as their existing users consumer more of their service.

Chewy describes the “embedded growth” in this existing customer base in their S-1 so we’re able to glean the following:

1) Overall Chewy’s customers continue to buy more stuff from them each year

Average revenue per customer has steadily increased from $223/yr in 2012 to $334/yr in 2018. We can infer this increase is due to some combination of Chewy broadening their selection of products over time and increasing brand loyalty by customers, yielding a higher share of wallet for pet-related spend. This is separate from the dynamics of any underlying cohort itself (more on that below).

2) Impressive cohort growth & stability

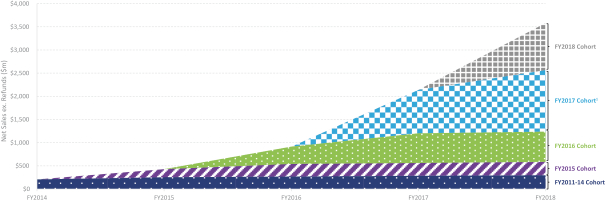

Chewy helpfully provides some cohort data on both aggregate $ revenue, active customer spend, and LTV/CAC basis. The first is most salient, as it tells us how much revenue Chewy generates from a particular cohort as it ages… it basically nets out effects of some customers dropping out with those that stick around buying more stuff. For example, Chewy’s 2015 cohort (e.g. customers who made their initial purchase in 2015) generated 165% of initial cohort revenue in 2018. In other words, for every $1.00 spent by new customers in 2015, that same group (in aggregate) bought $1.65 worth of goods from Chewy in 2018.

FWIW Chewy’s 2015 cohort appears to be their best one which is undoubtedly why they highlight it in the S-1, but other years demonstrate similarly strong persistence and growth based on the data they provide. Cohort revenue appears to grow significantly from first year to second year, and then largely levels off but persists for years.

Annual Net Sales By Customer Cohort

3) “Autoship” is a conveyor belt into consumers’ homes

While Chewy’s embedded growth ultimately comes from many consumers sticking around and increasing their spend over time, one of the drivers of this behavior is Chewy’s “autoship” model. While slightly more flexible than a simple monthly subscription (autoship customers also can make ad hoc purchases), the program lets consumers set recurring purchases for consumables they continuously replenish.

Customers in the autoship program generated roughly 66% of Chewy’s revenue in 2018. These customers also have a higher avg order value (AOV) than non-autoship customers, so they represent “better” customers for Chewy on multiple dimensions.

What Are Chewy’s Prospects for Profitability?

Chewy is unprofitable, on both a net income and EBITDA basis. Much of the press on the company’s IPO highlights this fact, which is easy to discern from a casual read of the S-1.

What I was curious to understand is what is the underlying potential for profitability for Chewy. How efficient is it as a business in terms of cash flow consumption or generation? Could Chewy reduce its marketing or other expenditures and be profitable now?

First, on an operating cashflow basis Chewy has been CF positive in some of the recent years. In 2016 they generated an operating cash profit of $7M, in a year where the company was still spending significantly on growth and grew revenue >100% YoY. In 2017 the company had an operating cash burn of roughly $80M, again in a year where the company did >$2B in revenue and grew >100% YoY. In 2018 Chewy was basically cashflow breakeven on an operating basis, with an operating cash burn of $13M on revenue of over $3B.

Operating cashflow represent the cash that’s generated or consumed by the business, excluding things like capital expenditures or year to year balance sheet changes in the level of inventories or payables. Chewy also appears to have cashflows going up to its parent PetSmart, which is owned by PE firm BC Partners. In the last two years cash has flowed both from Chewy to PetSmart and vice versa, but on a net basis Chewy has payed roughly $80M more in cash to PetSmart than has flowed from the parent company to Chewy.

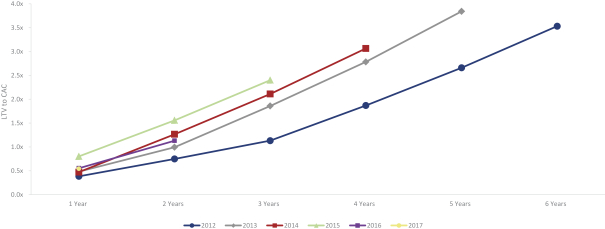

To put this all into context, in the past four years Chewy has consumed $134M (negative free cash flow) over the last four years while growing from $200M to $3.5B in revenue. Chewy has spent roughly $750M in marketing over the last three years to fuel growth, and while it has strong LTV/CAC ratios it still takes 1-2 years to see payback on its initial customer acquisition spend. In other words, if Chewy had cut all customer acquisition spend it would have solidly cashflow positive for several years albeit growing at a slower rate, though still growing given embedded growth described above.

Chewy LTV/CAC Ratios By Cohort Year

So If Chewy Is Fundamentally a Profitable Business, How Much Operating Leverage Exists?

We talk a lot about operating leverage in a business, e.g. the ability to increase various drivers of profitability which can make the business more profitable either on a unit basis or overall. To understand what operating leverage may exist in Chewy’s business, it’s helpful to first understand its existing profit margins.

Today Chewy’s underlying gross margins are just over 20%. Chewy cost of goods (COGS) includes both the underlying cost of the products sold but also some fulfillment related expenses like freight and packaging. Gross margins have been steadily improving in recent years from 16.6% in 2016, to 17.5% in 2017, and 20.2% in 2018 and according to the discussion in the S-1 much of this improvement has been attributable to higher product gross margin. Chewy has also started to introduce some private label brands, which presumably will drive higher product gross margin, though this is still fairly early in development. Chewy discloses that private label represents “mid single digit percentage” of sales, i.e. >90% of Chewy’s revenue is from selling 3rd party brands.

The other way we often look at margins is contribution margin. There can be genuine philosophical or accounting differences in how different costs are allocated, but generally I strive to think about a true “fully loaded” contribution margin. So for a commerce business like Chewy that would include:

Contribution Margin = (1) Net Revenue – (2) Product Cost – (3) Shipping – (4) Packaging – (5) Payment Processing Costs – (6) Direct Fulfillment Labor – (7) Variable Costs of Fulfillment Infrastructure

If you look at Chewy’s financials you’ll see a line item for Net Sales and a line item for COGS which includes #2, 3, and 4 above. But Chewy accounts for items #5, 6, and 7 within Selling, General, and Administrative (SG&A). They also include customer service costs in this Fulfillment bucket within SG&A, as well as some fixed (e.g. non-variable) costs associated with fulfillment.

Not all of the items #1-7 above are specifically provided in the S-1, so we have to infer based on the data Chewy does provides. We know that the total “Fulfillment” cost that Chewy accounts for in SG&A was just over $400M in 2018, so a bit over 11% of revenue. That includes items that appropriately would fall into contribution margin, like fulfillment labor (pick/pack/ship employees), payment processing costs (just shy of 20% of this Fulfillment bucket), and variable costs of fulfillment infrastructure like leases on warehouses. But there’s also probably some expenses in Fulfillment which are amortized fixed expenses for things like software or machinery in warehouses.

TLDR here is that it’s probably appropriate to add back a small portion of the expenses in the Fulfillment bucket Chewy reports in SG&A when trying to calculate fully-loaded contribution margin. So if you start with gross profit margin of 20.2% and subtract out the 11.4% in the Fulfillment cost bucket in SG&A, you get 8.8% which is probably a bit too conservative given it includes the amortized fixed expenses as I describe above. So it’s probably a fair assumption to say that Chewy has something like ~10% or slightly higher fully-loaded contribution margins, i.e. for every $1 of revenue roughly $0.10 in contribution profit is generated which can offset overhead and generate operating profit.

Conclusion

Bottom line, Chewy appears to be a pretty robust commerce business:

- It has a solid leadership position in a large and growing category

- It continues to grow rapidly, even at multi-billion revenue scale

- Chewy’s business is a “conveyor belt into consumers’ homes” with strong repeat purchase and growth LTV

- It’s core business is cashflow positive, excluding marketing spend for new customer acquisition

- It’s underlying gross margins and contribution margins appear to be steadily improving